The Demise of Cash in a New Normal Economy

With all this free money floating around, it's only so long before some serious inflation kicks in, and possibly a recession.

David Garner

How Covid Made the Rich Richer and Caused a Bubble that Will Pop Within 2 Years

Amidst the economic devastation bought on by Covid-19 in 2020. significant changes are afoot. The biggest transfer of wealth in recorded history is already well underway.

In this article you will learn how current monetary policy is making the rich richer, why cash is no longer king, and why an economic bust is not likely any time soon.

Invest for Safety: Check out our private lending program and start earning passive monthly income with the capital security of fully insured real estate

A Not so New Normal

At this point in American history, I think it is safe to say that the idea of “fiscal restraint” has become a quaint relic of the past.

It started in earnest in 2008. The US government and the Federal Reserve dumped more than $700 billion into big banks and Wall St. At the time, the voting public were sold the idea that these were simply loans. As it has turned out, these huge bailouts were in fact enormous transfers of wealth intended to preserve the wealth and power of government officials, billionaires, and investment bankers.

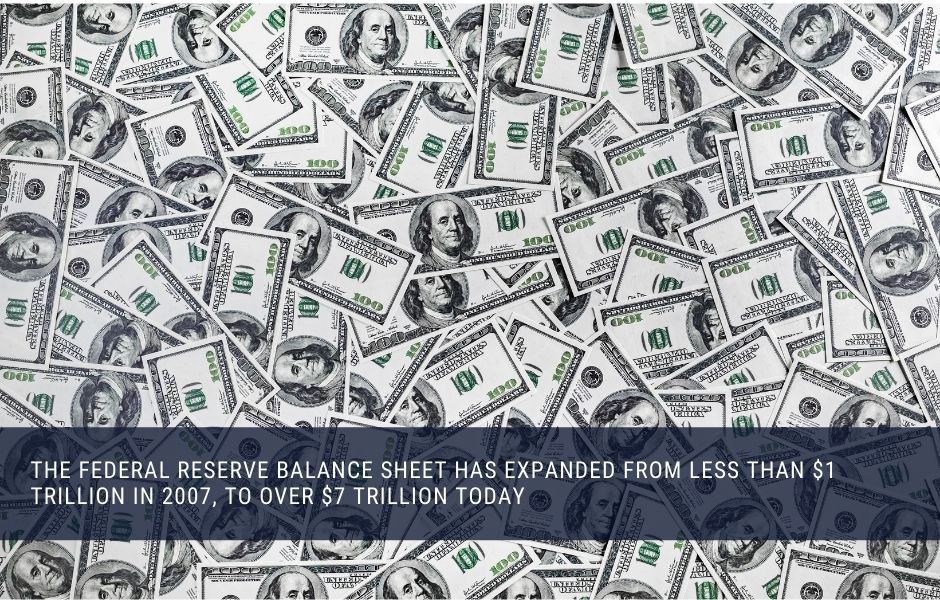

Today, trillion-dollar bailouts and near-zero interest rates are permanent fixtures in the policymaker’s playbook. In 2020 alone, the Federal Reserve printed an unfathomably enormous mountain of money to fund government spending on Covid-related stimulus programs. As a result, the Fed’s balance sheet has ballooned from less than $1 trillion in 2007, to over $7 trillion today.

A Gift to the Wealthy

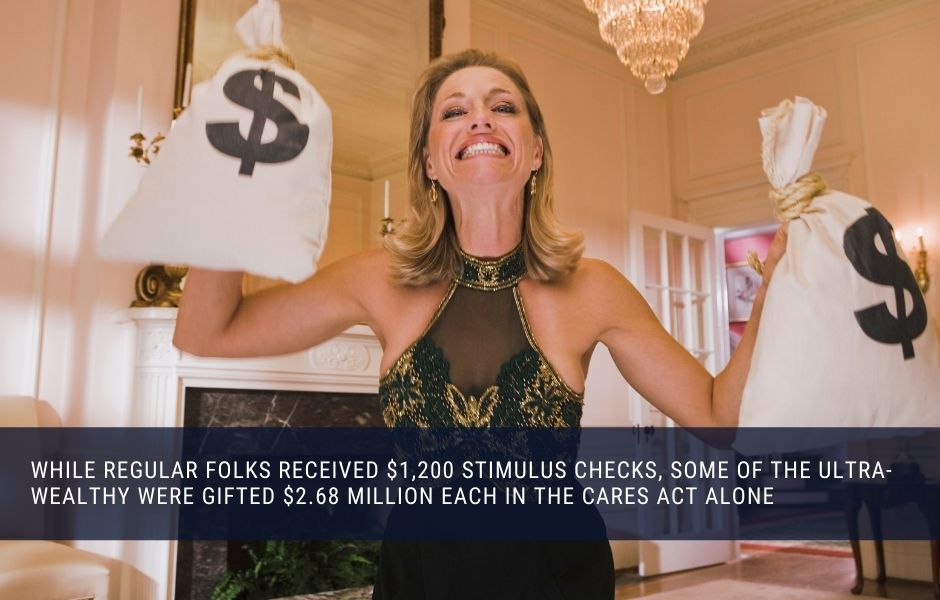

While a small portion of the Fed’s newly printed money came to regular folks (think, stimulus checks), far more has been handed to the wealthy.

Take the CARES Act for example. The IRS estimates it has sent out around 160 million stimulus checks worth over $270 billion. That’s an average of $1,687.50 per recipient.

What has not been discussed so publicly however, is the further $257.95 billion that was silently gifted to a much smaller number of wealthy individuals and families in the form of various tax breaks. This was worth much, much more.

The single biggest of these tax breaks will cost around $135 billion. This money helps people who own their businesses through partnerships or other similar structures who may have generated on-paper losses on their tax returns from their businesses.

But remember, just because they have losses for tax purposes, doesn’t necessarily mean they have a money-losing company. They could, actually, have a very profitable company.

This means that now, anyone earning over half a million dollars per year can use those on-paper losses to offset the taxes they might owe on, say, gains they have in the stock market separately, and crucially, to offset income that was taxed in previous years when tax rates were higher than they are now, AND get refunds based on those old, higher rates.

The Joint Committee on taxation (JCT) estimates that about 82% of these benefits — let’s call it $115 billion — will go to about 43,000 taxpayers with $1 million or more in annual income. That’s about $2.68 million EACH!

Slightly more than your $1,687.50!

Investment Opportunity: Click here to learn about our secured private lending program

Money Flows Upwards

To add insult to injury, the small amount of money that has made it into the hands of regular Americans has simply replaced lost household income. This money has also very quickly flowed back up to the rich in the form of rent and mortgage payments. It is the rich, after all, that own those assets too.

As the dust starts to settle on the US economy in 2021, one thing is obvious; the rich have gotten richer, and the poor, poorer. Wealth inequality – the uneven distribution of assets and income between rich and poor – has worsened at the fastest pace in recorded history.

Here is why that is important…

Joe Average spends their $1,687.50 on rent, mortgage payments, utilities, car payments, medical bills – all the usual stuff. Those receiving $2.68 million are using that money to buy more assets. And so, it is assets that have risen in value.

Not only do the rich get a bigger bite of the ‘free money pie’ they park that money in assets that are appreciating, exacerbating the divide between the have’s and the have nots.

The Relative Devaluation of Cash

For evidence of the inflationary impact of the Fed’s policies, one can look to house prices, or the correlation between the expansion of the Fed balance sheet and resultant growth of the S&P 500.

Ultimately, it is the average American who pays for all this, partly with higher taxes and government spending cuts, but mostly in the devaluation of our money. As the value of assets continues to rise, the relative value of cash diminishes by equal measure.

This is the reason millions of families can no longer afford to buy a home. You must spend more than double the amount of money on a house today compared to twenty years ago, or save twice as long or borrow twice as much.

This is also why the gap between rich and poor has never been so wide. There are those that own assets, and those that do not, and the longer you stay on one side of this divide, that harder it becomes to ever reach the other.

Unfortunately, there really is no escaping this coercive redistribution of income and wealth. Governments control money production, and people must use the governments’ money.

As investors, we must allocate our capital wisely to ensure we are on the right side of the transfer of wealth. We want to ride the wave of asset price inflation, not drown in a sea of worthless dollars.

Boom and Bust

Perhaps the most alarming consequence of expansive monetary policy is that artificial economic booms are set in motion. An increase in the money supply that is not backed by real savings pushes the market interest rate down. This discourages savings, increases consumption, and it also fuels additional investment.

Unfortunately, the boom brings overconsumption and malinvestment. People live beyond their means, consuming more and saving less. Investors make investments that would not be profitable under normal circumstances.

But so long as market interest rates remain artificially lowered through money printing, the boom is upheld. The problem occurs when the supply of excess new money dries up. Market interest rates returns to normal levels, and the boom quickly turns to bust.

Kicking the Can Down the Road

Of course, people love the boom, and they loathe the bust. So central banks can count on support from politicians, banks, industrial firms, unions, employees, and even pensioners to do whatever is necessary to keep it going. No one wants to pay the tab run up by the boom.

This leads central banks to bring interest rates even lower, and pump ever more credit and money into the system to keep the boom going. This keeps things going for a while, but it requires ever more “aggressive measures” to do so.

It does not take a genius to understand what this corrupt incentive structure brings. Central banks will keep inflating asset prices, because it supports the boom and they get away with it: people do not complain about “asset price inflation” and they do not blame central banks’ monetary policies for it.

And so it goes that the US dollar will most likely continue to lose its purchasing power over time. For those of us saving and investing for the future, or allocating our accrued wealth to generate income, the minimum advice is this: do not entrust your life savings to cash, invest in income for compound growth, and do not expect the crash just yet.

Investing 2021: Click here to learn about our secured private lending program