Note Investing 101 | The Ultimate Guide to Real Estate Mortgage Note Investing

Investor Bonus: See new mortgage notes for sale every Thursday

Mortgage note investing can be a great way to earn passive monthly income, or to acquire real estate at significant discount. In this article you'll learn everything you need to know to get started...

David Garner

Note Investing 101

Investing in real estate notes can be a great way to build wealth and generate income. But with many different types of mortgage note, investing strategies, and of course risks to consider, where do you start? In this article you’ll learn all the essential need-to-know basics to get you started on your own note investing journey!

Pro Tip: Get Details of NEW Mortgage Notes For Sale Delivered to Your Inbox Every Thursday

Contents:

- What is Note Investing

- My Experience With Real Estate Note Investing

- What Exactly is a Mortgage Note?

- Notes vs Real Estate Investing

- What are Notes Used For?

- What Every Note Investor Needs to Know

- Note Investing Strategies

- Where to Buy Mortgage Notes

- Note Investing Risks

- How to Get Started Real Estate Note Investing

- Real Estate Note investing 101 Video Series

This guide won’t make you an expert on note investing, but you will learn enough to get you started. I hope you find it useful. If you want to receive details of real estate notes for sale in your inbox every Thursday, join the Priority Investor Email below.

What is Note Investing?

Broadly speaking, note investing is the practice of purchasing real estate notes for the purposes of generating profits. that could mean profit from interest payments, or profits gained from the sale of the real estate or of the note itself. Of course, there’s a lot more to at than that. But in a nutshell, that’s it.

The three main reasons investors buy notes are:

- For the regular monthly income they produce

- The fact they are secured against physical real estate

- They can be purchased at a discount to the unpaid balance

Notes are commonly held by private investors in a self-directed IRA or 401(k). Typically they are used to boost and diversify retirement income, or improve overall returns. With interest rates stuck at historic lows, investors are seeking alternative investments capable of replacing lost income, and mortgage notes fit the bill quite nicely.

There are a few different ways to invest in real estate notes. You can buy them from banks, brokers, other note investors. There are even a few private note investment funds around too. Some investors also originate their own notes by providing private money loans direct to borrowers, or originating seller finance notes. Don’t worry, I’ll cover both of those later in this guide.

Liquidity and Profits

One huge benefit of mortgage notes over other types of real estate investing is the fact they are relatively liquid. Notes can be bought and sold freely on the secondary market, and you do not need to be an accredited investor with $100,000 to find good deals. This means note investing on the whole is accessible to all investors.

Perhaps the most attractive thing about investing in real estate notes is the potential for great returns without any of the hassle of real estate ownership. After all, lenders simply collect interest payments. They do not have to manage properties and tenants, or pay property taxes.

As I have alluded to already, every note is different, As such, your note investing strategy will vary from one note to another. You can buy income-producing notes, defaulted notes (known as non performing notes), notes with senior position liens, junior loans, and combinations thereof. Exactly what you do once you’ve acquired a note will depend on a number of variable specific to that paper.

My Experience With Real Estate Note Investing

My first introduction to note investing came in 2010, during the fallout from the global financial crisis. I was part of a team that acquired around $10 million of non performing notes from a very distressed bank for around $1 million. That’s’ 10 cent on the dollar!

We were able to ‘rehab’ most of the notes with the existing borrower and resell them at a significant profit. Where we couldn’t do deal like that, we foreclosed, took a deed in lieu, or arranged a short sale of the property.

This experience served as my introduction to the use of creative financing to sell homes, and planted the seed for the Pathway to Home Ownership Program we run today.

Making our 2010 investment profitable a LOT of work. But it was definitely one of the best investments I have ever been involved in… certainly in terms of ROI at least. The fact we were able to keep many families in their homes and avoid foreclosure was an added bonus!

Rebuilding America With Help From Note Investors

Today, I fund all my real estate investments with notes. I have about 70 long term rental property and rent to won houses right now in our Pathway to Home Ownership affordable housing program.

When I find a house that we want to own, one of my private lenders loans me the money for the purchase. So my investor acts as the bank, holding a note with monthly interest payments. Meanwhile, I get access to capital that allows me to close on the deal quickly, so I can typically out-manoeuvre the competition.

I’ve used this model working with notes to close on over 100 real estate investments since 2016. It’s been a fantastic way for us to scale our business, and a great way to earn passive monthly income for our investors!

Related: Learn About Our Investor Program

What Exactly is a Note?

When is a mortgage note not just a note? All the time, actually. We say ‘mortgage note’ or ‘real estate note’, but there are effectively two separate entities to consider; a promissory note (the actual “Note”) and a lien.

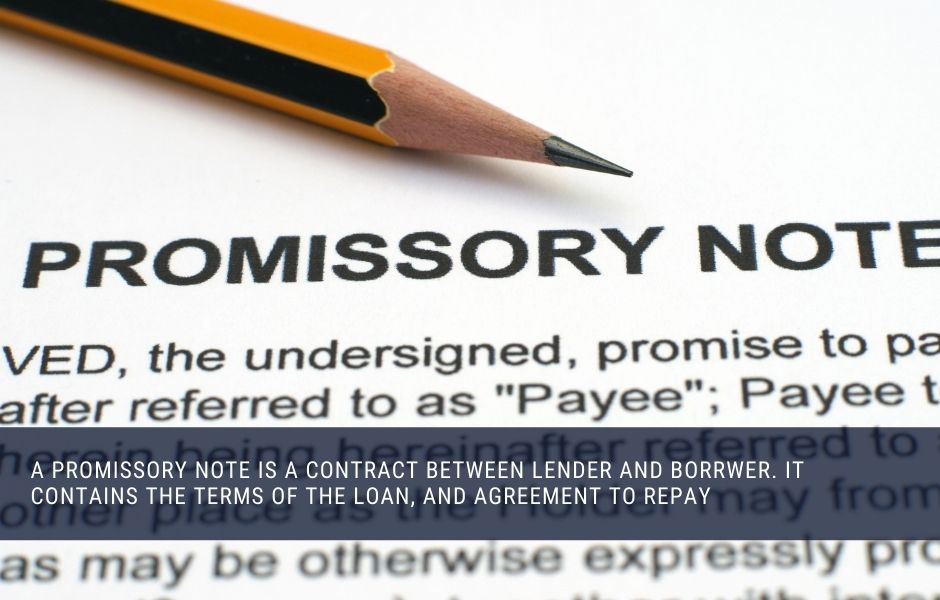

The Promissory Note

The note itself is a contract between the borrower and the lender This document states the amount of debt, rate of interest and term of the loan (among other things). The note also contains the terms of the investment such as balloon payments and what happens if the borrower defaults.

In the world of private mortgage note investing, no promissory note is created equal. Lenders set their own terms that are unique to each deal, and these can be quite different from one loan to another.

Related: What is a Note and What Terms Should it Contain?

The Lien

The second component of a ‘note’ is the lien. The lien provides you with security for your investment. This will be either a mortgage deed or deed of trust depending on which State the property is located in. Liens are recorded against the title to the property at the County records office.

If the borrower defaults on the terms of the note, for example if they fall behind on scheduled payments by more than 90 days, then the lenders may be able to use certain remedies detailed in the note to try and get their money back. These might include accelerating the loan, or starting foreclosure proceedings to force a sale of the property and settlement of their lien from the proceeds.

Liens can be recorded in 1st or 2nd position. If the property is sold, 1st position liens are usually settled first. This makes investing in 2nd position notes more risky, but potentially more profitable.

It is important to understand that you can still suffer a total loss of your investment even if your note comes with a 1st position senior lien. There are other liens that can take priority in a foreclosure such as some tax liens and other judgement liens. It can be a minefield, and not being aware of dirty title like this is an easy way to lose money.

Related: Everything You Need to Know About Lien Position and Priority

Real Estate Notes vs Rental Properties

As I mentioned early on in this article, being the bank takes far less effort than being a property owner. That’s why you’ll see many long-term real estate investors make the shift from owning and managing rental properties to real estate note investing instead.

One great example of this is Dave Van Horn – he literally wrote the book on note investing. He build a sizeable real portfolio, then switched out to note investing instead. Make no mistake, owning real estate can be very rewarding on many levels, but it takes time, effort, patience and resources to do it right!

Something I learned very early on in my real estate investing career is the importance of scale. If you’re going to own rental properties then – in my opinion – you need a lot of them! I have seen plenty of investors with just one or two houses end up selling up because they take up too much time, effort and money for not enough financial reward.

Today, these small scale rental investors are a great source of new acquisitions for me. As they sell off their assets at a discount, I’m there ready to buy, funded by my note investing partners. Seriously, I get calls on a weekly basis from people that bought turnkey rentals and now want out.

In my experience, you need at least 20 doors to ensure you have enough diversified rental cashflow to accommodate the big, unexpected costs that invariably crop up against individual properties, and to absorb vacancies in individual units. that’s a lot of houses, and it takes a lot of resources and personal financial risk to reach that level. It’s not for everyone!

This is true for me too. I personally own properties that looked like great deals when I bought them, but have never turned a cashflow profit due to continual capex and vacancies. Fortunately now I own enough to absorb the mistakes, but it definitely still happens.

Tenants can also be a costly issue. Even trees falling on houses, and theft of large items like furnaces or HVAC, or non-payment of rent. There are many ways to wipe out all your cashflow if you don’t own enough units to absorb individual losses.

My note investors on the other hand get paid their interest every month regardless of any issues with rent collections or maintenance. If the interest check doesn’t come in, they can ultimately foreclose the loan and I lose my asset.

Real estate is my full-time job. I have the time and resources to do things right. I have an exceptional team and I enjoy it. We have our own General Contracting Licence and regular, reliable crews on call 24/7. I have admin support, I have in-house property managers looking after rents and tenants, and I’ve partnered with some of the very best realtors that I have known for nearly 10 years.

I didn’t start out with all that help though. It has taken a huge amount of time, effort and money to scale my business to the point it is at now. I have gone through the pain of self managing a small number of properties, and it is hard! Mortgage note investing is way easier.

Related: Rental Properties – Investments That Pay Monthly Income

What are Notes Used For?

There are many more uses for mortgage notes then simply buying property. If you own real estate you can use a mortgage note to release equity for any reason. Here are some of the main uses of mortgage notes in real estate:

- Traditional mortgage loan (house purchase)

- Hard money loans

- Private money loans

- Home improvement/equity release

- Joint ventures investments

- Capital for business ventures

- Seller financing (House sale)

I have used notes for most of these things over the past 10 years. Sometimes we sell our houses with owner financing and then sell the note to cash out our investment. I also regularly work with private lenders who use mortgage notes to fund my acquisitions.

It is important to understand the original purpose of the note you are buying. Was it used to fund an acquisition, a renovation, or to fund something else completely unrelated to the real estate? These are important questions that will help you make better investing decisions when it comes to mortgage note investing.

Related: What Are Notes Used For? A More Comprehensive List

What Every Note Investor Needs to Know

If you’re going to buy mortgage note as an investment, the first thing to do is figure out your own goals. Do you want passive income with low risk? or big potential returns and/or losses? If you know what you’re looking for then you can find notes that fit your criteria.

When I’m buying a note, the first 3 things I ascertain are;

- Is the note performing?

- Is the lien 1st or 2nd position?

- Is the loan amortized?

If you are looking for passive income with little effort and low risk, you want performing notes with 1st position liens. If you want the potential for big profits with the potential risk of big losses, then you want heavily discounted non-performing notes. Of course, there is a lot more to it than that, but this is a good place to start.

Performing vs Non-Performing Notes

A mortgage note is performing when the borrower is current on payments. Performing notes are a great tool to diversify portfolio and collect passive monthly income with relatively low risk.

If the borrower is in default the note is non-performing. A note typically becomes non-performing when payments on the loan are overdue by 90 days or more. Non-performing loans are considered as bad debt because the chances of them getting paid back under the current terms are minimal.

Investors usually buy non-performing notes from other lenders at a discount to face value. Lenders and investors sell their non-performing notes to cash out quickly and avoid lengthy and costly foreclosure proceedings.

Once a non-performing note is acquired, the new lender will either attempt to modify the terms of the note with the borrower to get them paying again at some level, or simply foreclose the loan and sell the real estate. This takes time, effort and resources, and dealing with defaulted borrowers is no picnic. But, it can also be very profitable.

Related: Performing vs Non-Performing Notes – Which is the Better Investment?

Lien Position and Priority

As I already mentioned at the beginning of this post, There are 1st position and 2nd position liens. The position of the lien securing your note investment becomes critical if you have to foreclose the loan.

In a foreclosure, a 1st position lien takes priority over all other liens and is settled first from the proceeds of the sale. A 2nd position lien is a junior loan and is repaid only after the 1st position loan has been repaid in full. This makes 2nd position note investing much more risky.

[EXAMPLE] Assume a house sells for $100,000 (net of closing costs). There is a 1st position lien for $80,000 and a 2nd position lien for $35,000. The 1st position lender gets back 100% of their money, but in this case the 2nd position lender gets back only $20,000 of their $35,000 loan.

There are also other types of liens that could take priority over even a 1st position mortgage, including judgement liens and tax liens. Always make sure you do proper title checks before investing in any mortgage note. You could run the risk of losing all your money if there are other liens you do not know about.

Related: The Investors Guide to Lien Position and Priority

What is Amortization?

Amortization refers to how the repayment of both loan principal and interest is scheduled over time. There are 2 types of loan; amortized and interest only.

Amortized Notes

When a loan is amortized, each monthly payment consists of some interest and some of the principal loan amount. Amortized notes comes with an amortization schedule detailing how each monthly payment is apportioned between capital and interest.

It is important to understand that interest on an amortized loan is usually recalculated every month based on the most recent ending balance. So as each monthly payment reduces the principal balance, less interest becomes due. This means that the return on investment to an amortized note will be LESS than the interest rate, unless the loan is purchased at a significant discount to face value.

[EXAMPLE] A $100,000 mortgage note has an interest rate of 6 per cent (6%). The loan is amortized over 15 years. The borrower will pay back a total of $151,894 (180 payments of $843.86). This is a total interest income of $51,891 (52% ROI). That works out to a simple annualized return on investment of 3.46%.

Some notes can be amortized over a long period with a balloon payment set earlier on. For example, a loan might be amortized over 30 years to keep the monthly payments as low as possible, with a balloon payment for all outstanding principal at 10 years.

[EXAMPLE] A $100,000 mortgage note has an interest rate of 6 per cent (6%). The loan is amortized over 15 years. There is a balloon payment after 10 years. The total repaid to the lender over ten years would be $144,183. That’s 120 monthly payments of $843.86, plus a balloon payments of $43,023. This equates to a profit of $44,183 over ten years, or a simple annualized return of 4.42%.

Interest Only Notes

Where a loan is not amortized, 100% of every monthly payment consists of interest. The principal balance remains the same until it comes due at maturity of the note. I use interest only notes to fund my real estate investments. My private lenders much prefer a simple interest check and a balloon payment.

[EXAMPLE] A $100,000 interest only loan has an interest rate of 6%. Over 15 years, the borrower will pay will pay $90,000 in interest, plus repayment of the $100,000 principal at maturity. This is a fairly obvious simple annualized return on investment of 6%.

Making sure you understand how a loan is amortized is fundamental to note investing discovery and due diligence. There are pros and cons for both, and ultimately it will be your own personal investing objectives that define the type of note to invest in.

Related: The Essential Private Lending Investor Checklist

Loan to Value (LTV) and Investment to Value (ITV)

LTV and ITV are both key considerations for investors for note investors. The LTV (loan-to-value) shows the face value of the loan as a percentage of the collateral property value. A lower LTV indicates a lower risk of capital loss for the lender.

ITV (investment-to-value) is the purchase price of the mortgage note as a percentage of the collateral property value. The LTV and ITV will be different if you are buying the note at a discount. Again, the lower this ratio, the more equity is in the deal and less risk for the note investor in the case of a foreclosure.

[EXAMPLE] A house is worth $100,000 in as-is condition. There is a mortgage note with an outstanding balance of $75,000. In this case the LTV is 75%. If you were to buy the note for $50,000 then your ITV will be 50%.

An LTV/ITV of 65% or lower is generally considered decent as the lender is likely to be able to recoup all or most of the loan in the case of a foreclosure.

Remember, In order to figure out these key metrics you need to know what the underlying real estate is actually worth. I’ll talk about that in more detail later in this article.

Related: How to Value Real Estate for Private Lending and Note Investing

What is Seasoning?

Seasoning refers the length of time a borrower has been making payments on a note. A well-seasoned note is generally considered a more attractive investment as there is an established payment history with the borrower.

Term and Maturity

These terms are broadly interchangeable. Term is the length of time before the full balance on the note comes due. Maturity refers to the actual due date. Term to maturity is an important consideration in mortgage note investing. Most investors prefer shorter terms, with 15 years or less to maturity seemingly the benchmark for many.

What are Points?

Points are a form of upfront interest paid to the lender by the borrower. Hard money lenders in particular use points to increase their return on investment.

Points are calculated as a percentage of the loan amount, with 1 point being equivalent to 1% of the loan. Points should be rolled up into total interest in order to accurately calculate overall ROI from a note investment.

[EXAMPLE] A $100,000 note with a 3-year term has an interest rate of 6%. The lender charges 3 points to the borrower. The extra return in the form of points pushes the simple annualized ROI from 6% to 7%. Points are usually paid upfront at loan origination, but can also be charged annually at each anniversary of the note.

Loan Servicing for Note Investors

Whether you buy an existing note, or make a new loan, when you start note investing you will need to start collecting repayments. You can either collect payments direct from the borrower or use a loan servicing company.

A servicing company will manage and collect payments from your borrowers every month. They will record each payment, including the escrow amounts, and disburse the correct amount to the appropriate parties.

Additionally, a note servicing company has the resources and time to pursue late payments on a routine basis. If you are intending on doing a lot of mortgage note investing the collection process can become very time consuming and tedious, so a note servicing company is a good option.

While note servicing takes away a lot of the hassle, it also costs money. Remember, nothing comes for free, but a good service that save you time and effort, and keeps your records in great shape, is worth paying for.

Related: 5 Note Servicing Companies for Private Note Investors

Mortgage Note Investing Strategies

Investing in real estate notes can be very simple or very complicated depending on the the investment strategy you choose. First, you must decide on a strategy that suits your own investing goals. This will help to define your note investing criteria.

Performing Notes for Income

If you are looking for passive monthly income, then performing notes are for you. Performing notes are a great portfolio diversification and risk management tool for cautious investors, and the interest rates on private notes are far higher than current rates for CDs and other interest-bearing investments.

The income from performing notes can also be an amazing tool to grow your portfolio in the fastest way possible. Reinvesting income for compound growth is the most efficient way to grow your wealth fast. Because notes generate new income to reinvest every month, your growth compounds at the fastest possible rate.

If you’ve decided that performing notes are for you, you must then decide on your attitude to risk. This will further define whether you should look for 1st position or 2nd position note investments.

Notes with 1st position liens and a nice low (below 65%) LTV or ITV are considered low risk and carry a lower rate of interest. These types of notes trade at a premium due to the fact they are considered relatively safe investments.

Notes with a lien in 2nd position are considered higher risk, and this is reflected in a higher rate of interest. That said, every note investment is different, and overall risk is determined by a many more factors.

Related: 7 Mortgage Note Investing Strategies

Private Lending

Another way to use real estate notes to generate income, is to originate your own loans. I work with private lenders all the time. They loan me fund to buy and rehab rental properties, and I pay them fixed interest every month. It’s a great way for me to access quick cash to close a deal, and my lenders get a great rate of interest paid tax free into their IRA or 401(k).

Private lending has some interesting advantages over note investing. As a private lender you will have a much closer relationship with your borrower, and you will also likely have more input into the terms and structure of the note. Rates are pretty good at between 8% and 10%, and you should always be in 1st position.

Find Lending Opportunities: Absolutely Everything You Need to Know About Private Lending

Non Performing Notes

This is where things can start to get really complex. My first exposure to US real estate was in the purchase of a non-performing loan book from a bank in 2010, so I know how challenging – and rewarding – this can be.

Investing in non performing notes takes a lot of knowledge, time and effort to get right. I think it is true to say that way more people lose money investing in non performing notes than turn a profit. However, those who do make it work do very well indeed. I’ll cover some of the basics here.

Just like with a physical property, an investor will buy a non performing note and then either add value to it by getting the borrower paying again, or foreclose the loan and work out an exit strategy through the real estate.

If you successfully modify a non performing note to make it perform, you can keep it for the income or sell it for a profit. You can also sell part of the note (a partial) and keep some of the income, or you can borrow against the note to release your capital.

Non performing notes are so profitable because they are available to purchase at significant discount to the amount owning. I have bought non performing loans for as little as 10 cents on the dollar. Performing notes on the other hand can trade anywhere up to full price. So you see, there is a huge margin of value to add – if you can pull it off!

Three things you should bear in mind if you are considering an investment in non-performing notes;

- The amount of expertise and knowledge you need,

- The amount of time and resources it can take,

- The potential cash burn.

There are lots of companies out there selling non-performing notes. Sadly, many of these are just investors selling the trash they don’t want to new investors that don’t know any better.

There are also lots of ‘gurus’ selling note investing education. Again, tread carefully. There are plenty of people out there willing to take your coin on the promises of making you rich beyond your wildest dreams. Sadly, it never quite works out like that. There are good companies out there too of course, but make sure you do your due diligence!

Related: Non Performing Notes – Everything You Need to Know

A Word on Discounted Notes

This is important to understand from the outset of your note investing journey. On the secondary market, notes generally trade at a discount to the UPB (Unpaid Balance). This is a huge factor in calculating your return on investment, and is important when considering risk.

As with any asset, a note is only worth what someone is prepared to pay. There is a lot to take into consideration when deciding how much you are prepared to pay for a note. A note investor will make an offer that they feel reflects the risk and return attached to any given note.

Well-seasoned performing notes with a 1st position lien, low LTV, good collateral and solid borrower are considered the most stable assets. Investors will pay top dollar for these notes so they trade at – or very close to – UPB. in some cases I have even seen notes trade at a premium to UPB.

At the other end of the spectrum, you have non performing notes in second position with poor collateral and a bad (or absent) borrower. These notes trade at huge discounts to UPB because the amount of time, effort, resources and risk involved in working out the note or a foreclosure can be immense. But this is also what makes non performing notes so potentially profitable.

Common reasons for a discount can include;

- Current lender needs quick cash

- Borrower is in default (a non-performing loan)

- Questionable collateral (the quality of the property may have deteriorated since the loan was made)

- There are other liens (the borrower has gotten themselves into a credit hole)

- Property taxes are overdue (the property owner may have fallen delinquent on taxes, this could lead to a total loss for the lender)

- Other circumstances that might indicate a higher risk of lending at that time

If you are going to buy a discounted note, make sure to do your research and find out why it is discounted. Often you will find that the bigger the discount, the bigger the problem.

Notes For Sale: View Notes for Sale Right Now in our Self-Directed Investor Portal

Where to Buy Mortgage Notes?

So, you’ve defined your personal investment goals, worked out how much risk you are prepared to take, and decided on the type of mortgage note you want to invest in. Now, you need to actually get out there and buy mortgage notes.

Whether you are looking for performing notes for the passive income, or non-performing notes for the potentially bigger profits, there are actually plenty of places to buy mortgage notes if you know where to look. Here are some of the most common sources for mortgage note buying:

Buying Notes From Banks

When it comes to buying mortgage notes, the obvious place to start is the lender. Banks and other lenders sell both preforming and non performing notes, however as a smaller investor you are likely to find mostly non performing notes.

Buying notes from banks is a lot of work. It takes a lot of time and effort to identify sellers and build relationships with decision makers. Thankfully, there are some useful tools that will help you.

Bankprospector is a tool that will help you to identify banks and credit unions with non performing notes and REO to sell. By providing you with direct contact details for the seller’s decision maker, Bankprospector allows you to save a tremendous amount of time and effort, and cut out many of the middle men.

Related: My Ultimate List of Mortgage Notes For Sale

Online Exchanges

There are lots of online platforms where investors can buy and sell mortgage notes. Buying notes online is easy and accessible.

Here is a top 10 list of place to buy mortgage notes online:

- Garnaco Private Lender Portal

- Paperstac

- FCI Exchange

- Loan MLS

- Notes Direct

- Watermark Exchange

- Peer Street

- Lending Home

- Blackhawk Investments

- Fundrise

Remember, once something is publicly listed for sale you are likely going to be paying top price. This is no different for notes. If you buy notes from an online exchange you are paying retail, not wholesale prices.

Paying retail prices for notes is fine. The ease and accessibility makes somewhat makes up for the price premium, but any of the early stage value will already have gone.

Priority Investor List: Join 5,000+ private investors on our Priority Investor List, and get details of mortgage notes for sale in your inbox every Thursday

Become a Private Lender

If you are looking to generate passive income from note investing, the I would suggest becoming a private lender. In a private lending transaction, you originate your own note with a real estate investor. Effectively, you become the bank from day one, which means you get to set the terms of the deal.

For investors that want passive income, private lending carries a number of significant advantages over note investing:

- You get to set the terms of the loan yourself

- You get a direct relationship with your borrower (absolutely golden!)

- You get to assess the collateral in more detail

- You get to build a long term relationship for future investments

- There are no mark-ups or broker fees to pay

In my experience, having direct contact with the borrower can be extremely useful at both the due diligence stage (valuing the collateral property and assessing the borrower), and especially in the event of a default. Being able to speak to your borrower and understanding any issues surrounding a default is extremely valuable. This will help you tremendously when it comes to deciding whether to cut the borrower some slack or starting the process of foreclosure.

Related: See Private lending Opportunities Right Now in our Private Lender Portal

Working With Hard Money Lenders

If you cannot find a good private lending opportunity, or you would rather not be responsible for assessing a potential deal, then you can work with a hard money lender.

Hard money lenders are professional lenders who provide loans to real estate investors for acquisitions and renovations. They often use a combination of their own capital and investor money to make these loans, so they are always looking for passive investors to partner with.

As an investor, you can loan money to the hard money lender who will then use it to make a loan to a real estate investor. Or, in some cases you will make the loan directly to the borrower. Hard money lenders make their profits from upfront fees and interest rate arbitrage.

Passive investors rely of the hard money lender’s experience, leaving all of the lending decisions to them. Their business depends on them making good decisions for them and their investors.

Related: Top 4 Hard Money Loan Risks and Scams

Note Brokers and Hedge Funds

This is somewhat of a grey area. There is no shortage of ‘brokers’ and ‘hedge funds’ offering mortgage notes for sale. You should be vary careful when dealing with these middlemen, who are often referred to as ‘joker-brokers’ by more experienced note investors.

Brokers and hedge funds offering performing notes for sale most likely acquired the loans as non-performing and rehabbed the note. Selling these notes on to other investors is their exit strategy. You should be careful about the long term sustainability of these notes.

If a broker or ‘fund’ is selling non-performing notes, often it is the trash they do not want, or they are flipping notes they have bought wholesale from banks and other lenders.

Again, a note of caution is advised when dealing with middlemen. While everyone is in business to make a profit, you should be wary of those making a profit solely from selling notes to you and NOT from note investing themselves.

Related: How We Work With Private Lenders to Create Affordable Housing for Working Families

Investing in Note Funds

If you want the income and returns from mortgage note investing, but you want to be totally removed from the process, then it might be best to leave it to the professionals and invest in a note fund.

A note fund is typically a corporate entity operated by a fund manager who invests in mortgages. The fund raises money by selling shares, units or memberships, and that money is used either to buy mortgages on the secondary market, or is loaned out to a range of borrowers. Some funds might use the money to invest in other mortgage funds.

Note funds are a great hands-off way to get into note investing, but every fund is different. Each has their own remit, investing in different types of mortgages and borrowers. The fees charged by fund managers also vary significantly from one note fund to another.

Two things to consider with mortgage funds are accessibility and liquidity. Access to these types of funds is often reserved only for accredited investors with large sums to invest, whereas anyone can buy or sell an individual note. Also, an individual mortgage note can be sold easily if you need to liquidate, however shares or units in a note fund often have strict restrictions on sale and liquidity.

Related: Top 5 Mortgage Note Investment Funds for 2021

Mortgage Note Investing Risks

While note investing can be a great way to diversify your investments and generate regular income – nothing is without risk. Because there are so many investment strategies for investing in notes, the level of risk you take will ultimately be defined by the type of note you purchase, and what you intend to achieve with it.

As I have already mentioned in this article, note investing risk is a spectrum. At the lowest risk/highest value end there are performing notes with a 1st position lien, a good borrower and solid collateral. At the other end of the spectrum sit non performing notes in 2nd position with questionable borrowers and issues with collateral (value and/or title).

All that said, every note carries some risk, and the return should reflect that. The process of underwriting a note investment to establish appropriate premiums, discounts and interest rates involves assessing both the borrower and the collateral.

Borrower Quality (Credit Risk)

Understanding the ability of your borrower to meet loan repayments is fundamental to underwriting a note investment. The terms you set when modifying a non performing note or writing a new private lending deal should reflect the risk of the borrower defaulting.

Where the note is secured against an owner-occupied property, obtaining a credit score is a good start. A score of 550+ is broadly accepted as a starting point of creditworthiness. You may also want to get an idea of their debt-to-income ratio.

Of course, some of this information may not be available right away when purchasing a note. You might have only very basic information available such as borrower credit score and approximate collateral valuation, so you must use these as best you can to help define the price you are willing to pay.

For loans made against rental properties, you will want to look at rental income and debt repayments. This is known as the debt service coverage ratio or DSCR. DSCR is calculated as the ratio of net operating income (NOI) to the debt repayments. The higher this ratio is, the lower the risk associated with the note.

Related: The Essential Guide to Credit Risk for Private Lenders and Note Investors

Real Estate Valuations for Lenders and Note Investors

Real estate notes are secured against physical property. Ultimately, it is the real estate that provides a backstop for your investment in a worst case scenario, so you want a good idea of the disposal value.

It seems obvious to say, but the more valuable the real estate in relation to the loan amount the better!

There is more to this than a simple appraisal. There are lots of factors that affect the net disposal value of a piece of real estate. Physical condition and general market conditions are one thing, but you must also pay close attention to the condition of the title. You do not want to be stuck up owning a house awash with liens that could take priority over even a 1st position mortgage in a foreclosure.

Related: The Guide to Real Estate Valuations for Private Lenders

How to Get Started in Note Investing

I hope this article has been useful. It certainly took a while to write and edit. As I mentioned right at the beginning, this guide is not intended to make you an expert at note investing, but the information laid out here is a good start. If you have skipped to this section from the contents list, go back and read it from the start – it will help, I promise.

So, how do you get started in mortgage note investing? Well, first you need to figure out what you want to achieve and what risk you are prepared to take. Are you looking for passive income with minimal risk? or do you want to risk more and go for the big wins? The section on note investing strategies can help you with that!

You also need to continue with your education. That is a constant. The note investing game is very complex and brimming with nuance. Find yourself a mentor if you can, and when it comes to making your first note investment, start small.

Remember, note investing won’t make you rich overnight. Be wary of ‘educators’ that charge thousands of dollars for note investing courses. They are generally making their money from the fees you pay, not from actually investing in notes themselves. All of the information you need is already out there in the public domain.

P.S. I put together a series of videos covering real estate note investing in more detail… if you’re interested, I’ll post them below as I complete each episode, so make sure you keep checking back for updates.

If you prefer for me to keep you updated as I post more content, and to see details of the deals I’m doing myself every week, you can Join as a FREE Member of our Priority Investor Community right here.

Real Estate Note Investing 101 Video Series

Episode 1 – The Basics

In this presentation, I provide a very basic introduction to real estate note investing, and talk about some of the main reasons investors choose real estate notes over physical real estate, and introduce the 3 P’s; Paperwork, Property and Payor.

Some More Note Investing Articles

- Where to Buy Mortgage Notes – A Complete List of Verified Sources

- Note Investing 101 – Everything you Need to Know About Note Investing

- Private Lending 101 – The Complete Investors Guide to Private Money Lending

- How to Invest in Notes – 7 Note Investing Strategies

- What is a Note and What Terms Should It Contain?

- Performing vs Non-Performing Notes – Which is the Better Investment?

- The Private Lender’s Guide to Assessing Credit Risk

- Understanding Lien Position and Priority

- How to Buy Mortgage Notes Online in 2021

- How to Assess Real Estate for note Investing and Private Lending

- Find Performing Notes for Sale in 2021

- Private Lending 101 – Everything you Need to Know About Private Money Lending

- Is Buying Mortgage Notes a Good Investment in 2021?

- Note Investing vs Rental Properties – Which is the Best Investment?

- Performing Notes – What Why and How to Buy

- Is Real Estate Note Investing Risky?

- Real Estate Notes vs REITs – Which is the Better Investment?

- The 3 Best Real Estate Investing Opportunities in 2021

- What is the Difference Between a Note and a Mortgage?

- Real Estate Notes – Everything You Need to Know

- My Top 5 Real Estate Note Investing Tools and Resources

- 3 Note Investing Funds for Passive Investors

- Using Note Investing to Boost Your Monthly Income

- Non Performing Notes – Everything You Need to Know