Foreign National Mortgage Documents & KYC Checklist (2025)

David Garner

David Garner

David Garner

David GarnerForeign National Mortgage Documentation & KYC Checklist (2025 Guide + Templates)

Having purchased over 120 rental properties in the U.S. as a foreigner, I’ve learned a thing or two about mortgage financing for foreigners in the USA. Today, I help clients from all over the world build their own rental property portfolios in the U.S., and foreign national mortgages are the cornerstone of our financing strategy. In this guide, you’ll find everything you need to get approved for a foreign national loan in 2025.

What Lenders Verify (ID, Source of Funds, Reserves)

If you’re buying property in the USA as a foreigner, you’ll most likely need some kind of mortgage. But when you apply for a foreign national mortgage, the exact documents you need to provide for underwriting vary depending on the type of loan you need.

For full-doc conventional loans, lenders underwrite you (income, tax returns, credit). For Foreign national DSCR loans, lenders primarily underwrite the property’s cash flow; personal U.S. income and credit are generally not required (some programs may still ask for basic credit references). Here’s a breakdown of documentation requirements and guidelines by loan type:

All programs verify the following

- KYC/OFAC (identity & compliance): Passport/visa, sanctions screening, proof of address, and if using a corporate entity to purchase, then there will be additional entity checks.

- Source of funds: 90–120 days of statements showing accumulation of funds and incoming transfers; invoices/settlements for large deposits; wire receipts.

- Reserves: Typically 6–12+ months mortgage payments (often higher for short term rentals (STRs), 5+ units, or jumbo balances).

- Entity docs (if closing in an LLC): Articles/Operating Agreement, EIN letter, manager/member listing (state/title rules vary).

DSCR Documentation Requirements

- Property income: Current lease or 1007 market rent schedule (appraisal); STR addendum or booking history if using short-term rental income.

- Reserves & liquidity: Typically 6–12+ months mortgage payments (PITIA); higher for STRs, 5+ units, jumbo loans.

- KYC/OFAC & source-of-funds: As above; clean, dated trail from origin to escrow.

- Entity docs (if LLC): As above; a personal guarantee is a common requirement.

Conventional (Full-Doc) Documentation Requirements

- Credit: Credit report typically required; some foreign-national programs accept international credit or bank/reference letters.

- Personal income: Pay stubs, tax returns, bank statements, and verification of employment (VOE). If self-employed: CPA letter/financials.

- Translations: Non-English documents usually need certified translations.

- Assets & reserves: 2–6+ months PITIA (more with multiple financed properties or risk factors).

- KYC/OFAC, source-of-funds & entity (if applicable): Same as above.

Quick tip: Start compiling reserves and a clean source-of-funds trail before you request quotes. Not having this in place is a big cause of approval delays. For a step-by-step process for DSCR loans, see the Pre-Approval Checklist.

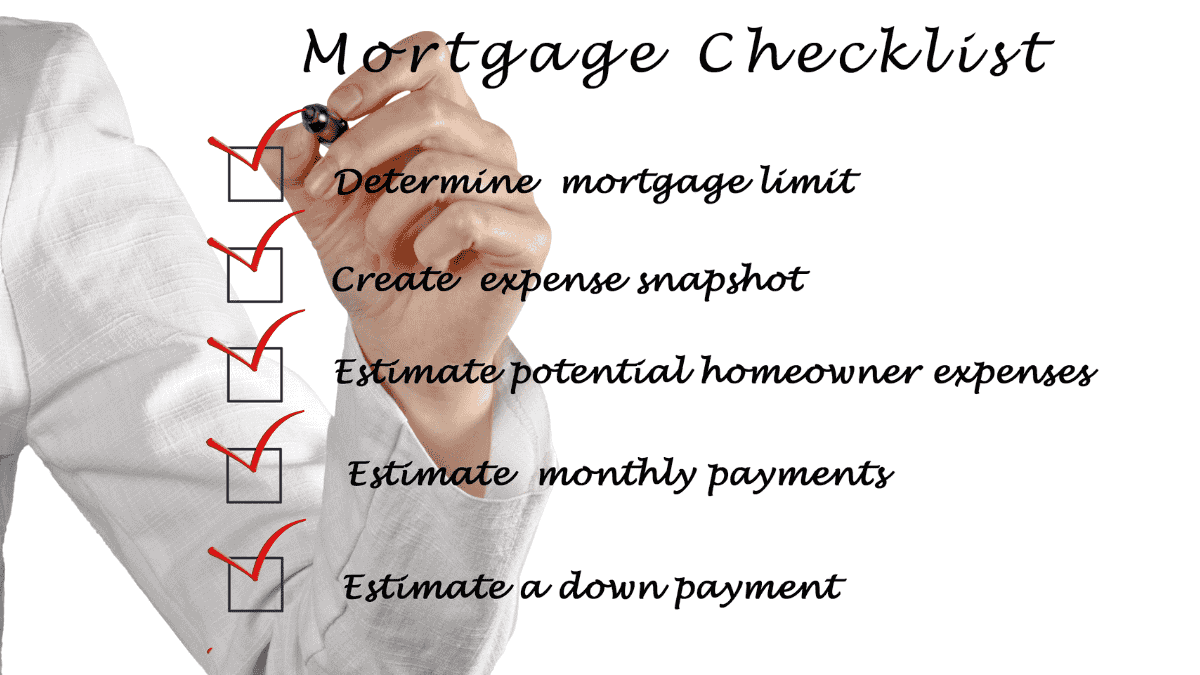

Documentation Checklist by Loan Type

The core KYC/OFAC and source-of-funds items are the same across most foreign national loan programs, but the proofs you submit differ by loan type. Use this checklist to assemble your documentation ahead of time and avoid delays and rework.

Foreign-National Mortgage Documentation — By Loan Type

| Item | Conventional (Investment) | DSCR (Foreign National) | ITIN (Investment) |

|---|---|---|---|

| Government ID | Passport/visa; secondary ID if requested | Passport/visa; secondary ID if requested | Passport/visa + ITIN assignment letter |

| Credit | U.S. credit report required; score-based pricing | Possible without U.S. credit; foreign credit/bank refs accepted in some programs | No SSN; ITIN file acceptable (stricter overlays) |

| Income | Pay stubs, tax returns, bank statements; VOE (employment verification) | Lease or 1007 market rent; STR addendum/booking history if using STR income | Alternative/foreign income docs; CPA or bank letters |

| Assets / Reserves | ~2–6+ months PITIA typical (more with multiple financed properties) | ~6–12+ months PITIA common; higher for STRs, 5+ units, or jumbo | ~6–12+ months PITIA common; lender may require more |

| Entity (LLC) | Usually personal title for 1–4 units | LLC allowed with personal guarantee (state/title/insurance rules) | LLC possible; lender-dependent |

| Source of Funds | 90–120 days statements; wire receipts; gift letter rules | KYC/SOF trail: statements, invoices/settlements, wire receipts | KYC/SOF trail: statements, invoices/settlements, wire receipts |

| Property Docs | Appraisal; condo/HOA docs if applicable | Appraisal + 1007 rent schedule; STR addendum if applicable | Appraisal; condo/HOA docs if applicable |

| Insurance & Taxes | Insurance binder; tax bill/estimates | Insurance binder; tax bill/estimates | Insurance binder; tax bill/estimates |

| Translations | Non-English docs need certified translations (if requested) | Non-English docs need certified translations (if requested) | Non-English docs need certified translations (if requested) |

JOIN MY VIP PRIORITY INVESTOR LIST

Get the Best Foreign National Mortgage Deals and Off-Market U.S. Investment Properties in Your Inbox Every WeekYES! ADD ME TO THE PRIORITY INVESTOR LIST

How to Prove Source of Funds (Templates)

Lenders need a clear, dated trail showing where your money came from and how it moved into escrow. Aim for 90–120 days of statements, consistent balances, and receipts for any large or unusual deposits.

- Time window: Provide the last 90–120 days of bank statements for all accounts funding the deal.

- Name match: Account holder name(s) must match your passport or your LLC (if vesting in an entity).

- Large deposits: Include invoices, sale/settlement statements, or payroll slips; add wire/transfer receipts.

- Path of funds: Show the chain (e.g., Brokerage → Checking → Title/Escrow); include intermediate statements.

- FX & wires: Keep bank confirmations and currency exchange receipts; send a test wire when possible.

- Gifts (if allowed): Provide a signed gift letter, donor bank statement, and transfer receipt; confirm seasoning rules.

If you’re going it alone rather than working with a mortgage broker, you can copy and paste the following templates for source of funds, bank balance, and proof of gifts.

Source-of-Funds Letter (Mini-Template)

To Whom It May Concern:

I, [Full Name] (passport [Number]), confirm that the funds used for the U.S. property purchase at [Property Address] derive from [employment income / business income / sale of asset / savings] and are held at [Bank Name, Country].

Enclosed are [90/120] days of statements and transfer receipts evidencing the accumulation and movement of funds.

I certify these funds are my own and are not borrowed.

Signed, [Full Name] Date: [MM/DD/YYYY]

Bank Balance Letter (Mini-Template)

To Whom It May Concern:

This is to confirm that [Client Name] (passport [Number]) maintains deposit accounts with [Bank Name].

As of [Date], the combined balance of accounts ending in [XXXX] is [Currency and Amount].

This letter is provided at the client’s request for mortgage underwriting purposes.

Signed, [Bank Officer Name] — [Title], [Branch/Contact]

Gift Letter (Mini-Template, if permitted)

I, [Donor Full Name], confirm an irrevocable gift of [Amount and Currency] to [Borrower Full Name] for the purchase of the property at [Address]. No repayment is expected. Supporting donor bank statement(s) and the transfer receipt are enclosed.

Donor Signature: _______________________

Date: [MM/DD/YYYY] Relationship: [Relation]

- Avoid: Cash deposits without documentation, screenshots that don’t show names/dates, or cropped statements without running balances.

- Pro tip: If you plan a cash-out refi within 6–12 months, keep before/after photos and paid invoices for any renovations—they support valuation/seasoning later.

Wire Transfers & Currency (Timeline & Pitfalls)

Sending money cross-border has never been easier, but there are still a few things to bear in mind. International wires can add days to your closing timeline. You should plan your transfers early, keep the name trail clean, and verify escrow details by phone before you send a large wire. Unfortunately, there are a lot of bad actors and lending scams out there, so be very careful to whom you send your money!

- Timing: International wires commonly take 1 to 3+ business days. Add a buffer for compliance reviews and intermediary banks.

- Cut-off times: Most banks have same-day cut-offs (often 2 to 4pm local). Miss it and your wire posts the next business day.

- Name match: Sender name must match the borrower/entity on contract. Third-party wires are often rejected.

- Purpose line: Ask your bank to include “Real estate purchase – escrow #” in the wire message to speed review.

- KYC/OFAC holds: Large or first-time wires can trigger manual review. Have your passport, source-of-funds docs, and invoices ready.

- FX strategy: Consider pre-funding USD or using a forward/lock with your bank or a licensed FX provider; avoid last-minute conversion risk. I use Wise for my own international money transfers.

- Fees & intermediaries: Expect sending + intermediary + receiving fees; send a little extra to avoid shortfalls in escrow.

- Wire fraud safety: Always phone-verify escrow instructions using a known number. Ignore “revised” instructions sent by email/text.

Closing timeline cheat-sheet:

- 10–7 days out: Request escrow wiring instructions; do a small test wire (e.g., $100) if allowed.

- 5–3 days out: Initiate your main wire; keep confirmations/screens with reference numbers.

- 2–1 days out: Confirm receipt of your funds with the title/escrow company; be prepared to top-up if fees reduced the net amount.

- Closing day: Re-verify any last-minute changes by phone, never rely on emailed instructions alone.

- Pro tip: If you intend to refinance or a cash-out later, keep a simple “Funds Trail” file (statements, wire receipts, invoices). It will help to shorten future underwriting timelines.

Common Rework Triggers (How to Avoid Delays)

In mortgage applications, “rework” refers to when a lender requests additional information or corrections to your application, sending it back to you for further action. When you’re applying for foreign national mortgage, there are likely to be some bottlenecks and delays, but most slowdowns are preventable. You can use this list to pre-empt the usual underwriting queries and keep your file moving.

- Unexplained large deposits: Any spike in the last 90 to 120 days needs a paper trail (invoice, sale/settlement, payroll). Add wire receipts.

- Name/entity mismatches: Passport name ≠ bank account ≠ purchase contract ≠ LLC docs. Align spellings and roles; include Operating Agreement + EIN if using an LLC.

- Insufficient reserves: Foreign-national and DSCR files often need 6 to 12+ months PITIA (more for STRs/5+ units/jumbo). Top up early or show additional accounts.

- Missing STR support: If qualifying on short-term rental income, include the STR addendum or booking history + 1007 market rent. HOA/municipal STR rules if requested.

- Translation gaps: Non-English statements or letters usually need certified translations. Provide both original and translated PDF.

- Wire timing & shortfalls: Late wires (cut-off missed) or net funds reduced by FX/fees. Initiate 3 to 5 days early and send a small test wire if allowed.

- Insurance/coverage issues: Binder missing the correct vesting (LLC vs personal) or inadequate dwelling/landlord coverage. Ask the carrier for a lender-compliant binder.

- Appraisal surprises: Access delays, STR comps not addressed, or condo/HOA docs slow to arrive. Schedule early and coordinate HOA documents up front.

- Credit/reference gaps (conventional only): Missing U.S. credit or insufficient trade lines—provide international bureau report or bank/reference letters if permitted.

Fix-fast playbook: Bundle docs into labeled PDFs (e.g., 01_ID.pdf, 02_SOF.pdf, 03_Reserves.pdf, 04_Entity.pdf), match names across all files, and add a 1-page “Funds Trail” cover sheet explaining the flow of money. For a step-by-step process for DSCR loans, see my Pre-Approval Checklist.

Next Steps

I highly recommend working with an experienced mortgage broker who can help you qualify for a foreign national loan, and handle all of the underwriting and documentation process for you.

I work with some amazing brokers that truly understand the rules, guidelines, and requirements for foreign national borrowers. If you’d like to connect with my personal broker specializing in foreign national loans, you can use the “Get Pre-Approved Today” button below. If you’re not ready to get pre-approved just yet, you can stay informed about the best foreign national mortgage rates and U.S. property investment deals by joining my VIP Priority Investor List.

GET PRE-APPROVED FOR YOUR FOREIGN NATIONAL LOAN

Start your real estate investment journey today, and get pre-approved for the best mortgage rates and terms for foreign national by market leading lenders!

“Having personally invested in over 120 US rental properties from overseas, I know the true value of getting the right advice and support.

David Garner – Cashflow Rentals

")

GET PRE-APPROVED FOR YOUR FOREIGN NATIONAL LOAN TODAY!

Start your real estate investment journey today get pre-approved for the best foreign national loan rates from market leading lenders!

“Having personally invested in over 120 US rental properties from overseas, I know the true value of getting the right advice and support.

David Garner – Cashflow Rentals

FAQs

Do I need U.S. credit or an SSN to get a mortgage?

Not always. Foreign-national DSCR programs can approve without U.S. credit or an SSN; ITIN loans work for investors who file with an ITIN. Expect overlays on LTV, pricing, and reserves, and be ready with bank/reference letters if requested.

How many months of reserves do lenders typically require?

Plan for 6–12+ months of PITIA. STRs, 5+ units, jumbo balances, and foreign-national files often sit at the higher end. Stronger reserves can also unlock better pricing or flexibility on property type.

What counts as acceptable proof of source of funds?

Provide 90–120 days of statements showing accumulation, plus transfer/wire receipts. Document large deposits with invoices or sale/settlement statements, and make sure account names match your passport or LLC.

Can I buy in an LLC as a non-U.S. resident?

Often yes with DSCR lenders; a personal guarantee is common. Title/insurance/state rules vary, so confirm vesting early and have Articles/Operating Agreement and EIN ready.